In the intricate realm of business operations, the role of meticulously chosen insurance cannot be overstated. It serves as a protective shield, a financial fortress that fortifies the enterprise against unforeseen adversities. The discerning business owner recognizes the indispensable nature of insurance, understanding that it is not merely an option but a crucial necessity. Delving into the nuanced facets of this decision unveils a labyrinth of possibilities, demanding a judicious selection process that harmonizes with the unique characteristics of each business. This article will give an overview of Insurance for business and how it can secure you from business risk.

Tailoring Insurance to the Nuances of Small Enterprises

Owning a small business catapults the imperative for business insurance to the forefront. The nuances of each enterprise, however, render the selection process a delicate art. It is not a one-size-fits-all scenario; rather, it metamorphoses into a bespoke garment, intricately tailored to the specific contours of the business at hand. The spectrum of available insurance types unfolds, presenting an array of options that can either fortify or falter depending on how well they align with the intricacies of the business’s nature and activities.

The Varied Landscape of Business Insurance

The landscape of business insurance is as diverse as the myriad of enterprises it seeks to safeguard. A meticulous examination reveals that not all insurance policies are created equal. They diverge significantly, reflecting the kaleidoscope of industries and their unique challenges. Whether one’s business is entrenched in manufacturing, services, or technology, the requisite insurance coverages differ drastically. From liability protections to property insurance, the entrepreneur is confronted with a plethora of choices, each bearing distinct implications for the safeguarding of the business’s interests.

Understanding the Fluid Dynamics of Business Activities

The pivotal factor in this labyrinthine decision-making process lies in comprehending the fluid dynamics of business activities. The type of insurance required becomes a dynamic equation, influenced by the ebbs and flows of the industry, market trends, and the inherent risks associated with specific business operations. Thus, the astute business owner navigates not only the static considerations of the present but anticipates the undulating nature of future uncertainties, strategically aligning insurance choices with the ever-evolving landscape of their enterprise.

Decoding the Essentiality of Business Insurance

In the grand tapestry of business ownership, the thread of insurance is woven seamlessly, binding together the warp and weft of financial security. Its essentiality transcends mere compliance; it becomes a proactive measure, a strategic investment in the resilience of the business. The conundrum of selecting the right insurance is, therefore, not a mere choice but a profound decision that shapes the contours of a business’s destiny. It requires a judicious blend of foresight, industry insight, and a nuanced understanding of the intricacies that define each business, ultimately culminating in a safeguarding mechanism that stands resilient in the face of uncertainties.

Unveiling the Reality of Business Risks

Many young entrepreneurs fall into the common trap of assuming that once their business is incorporated, they are shielded from potential risks. This misconception can prove to be a costly error. Small business owners should not rely solely on incorporation for protection, as legal issues can still arise. A false sense of security can lead to devastating consequences, as demonstrated by a personal anecdote from my own experience.

Small business insurance is a vital component of comprehensive business coverage. Even if you believe the risks to your business are identifiable and avoidable, this assumption might be rooted in a fundamental misunderstanding of how businesses operate. An illustrative example is my software business, where an employee inadvertently caused an explosion at a laundromat. This unforeseen incident nearly resulted in the loss of my entire company. Such unpredictable events underscore the importance of having robust insurance coverage to mitigate unforeseen risks.

How Insurance can secure you from business risk? 8 Insurance Pros

In the dynamic landscape of business, where uncertainty looms large and risks are an inherent part of the entrepreneurial journey, insurance emerges as a stalwart shield against potential adversities. Let’s delve into the intricacies of how insurance can provide a robust layer of protection, offering not just financial security but also peace of mind to business owners.

1. Cybersecurity and Data Breach Protection

In the digital age, the risk of cyber threats and data breaches is omnipresent. Cyber insurance has emerged as a crucial tool in safeguarding businesses from the financial fallout of such incidents. From covering the costs of data recovery to managing legal liabilities and reputational damage, this insurance not only secures digital assets but also instills confidence among customers and partners regarding the business’s commitment to cybersecurity.

2. Professional Liability Insurance

For businesses that provide professional services, the specter of professional liability is a constant concern. This type of insurance, also known as errors and omissions insurance, protects professionals from claims of negligence or inadequate work. It covers legal defense costs, settlements, and judgments, allowing professionals to navigate their responsibilities with confidence, knowing they have a safety net against unforeseen challenges.

3. Customized Coverage for Unique Risks

Every business is unique, with its own set of risks and challenges. One of the often overlooked advantages of insurance is its flexibility to be tailored to the specific needs of a business. From specialized coverage for niche industries to endorsements that address unique risks, entrepreneurs can work with insurers to create a bespoke insurance portfolio that aligns with their business model, providing a comprehensive safety net against a wide array of potential threats.

4. Financial Safeguard Against Property Loss

One of the primary advantages of business insurance lies in its ability to provide a financial cushion against property loss. Whether it’s a natural disaster like a flood or fire, or an unfortunate incident of theft, having comprehensive property insurance ensures that the financial burden of rebuilding or replacing assets doesn’t fall solely on the shoulders of the business owner. This, in turn, facilitates business continuity, preventing a single catastrophic event from causing irreparable damage.

5. Liability Protection

Business operations inherently carry the risk of liability, and a single lawsuit can potentially jeopardize the entire enterprise. Liability insurance becomes a critical asset in such scenarios, covering legal expenses and settlements. From customer injuries on the premises to product liability claims, having the right insurance coverage ensures that the business remains resilient in the face of unforeseen legal challenges, allowing entrepreneurs to focus on growth without the constant threat of litigation.

6. Employee Welfare with Workers’ Compensation

The workforce is the backbone of any business, and their well-being is paramount. Workers’ compensation insurance steps in to protect both employees and employers in the unfortunate event of work-related injuries or illnesses. By covering medical expenses and lost wages, this insurance not only safeguards the financial interests of the affected employees but also shields the business from potential lawsuits arising from workplace accidents.

7. Business Interruption Coverage

Disruptions to business operations can arise from a myriad of unforeseen events, such as natural disasters, equipment failure, or supply chain disruptions. Business interruption insurance becomes a crucial component in mitigating the financial impact of such disruptions. It compensates for lost income during downtime, covers ongoing expenses, and aids in the swift resumption of operations, minimizing the long-term effects of unexpected setbacks.

8. Key Person Insurance

In many businesses, certain individuals play pivotal roles that significantly contribute to the company’s success. Key person insurance ensures that the business can weather the storm caused by the loss of such indispensable individuals. Whether it’s the founder, a top-performing executive, or a key salesperson, this insurance provides financial support, allowing the business to recruit and train replacements and maintain its momentum during challenging times.

In summary, the realm of business insurance is a multifaceted landscape offering a diverse array of protections. From shielding physical assets to safeguarding against legal liabilities and embracing the digital age’s challenges, insurance stands as a formidable ally in the entrepreneurial journey, assuring that businesses can navigate uncertainties with resilience and confidence.

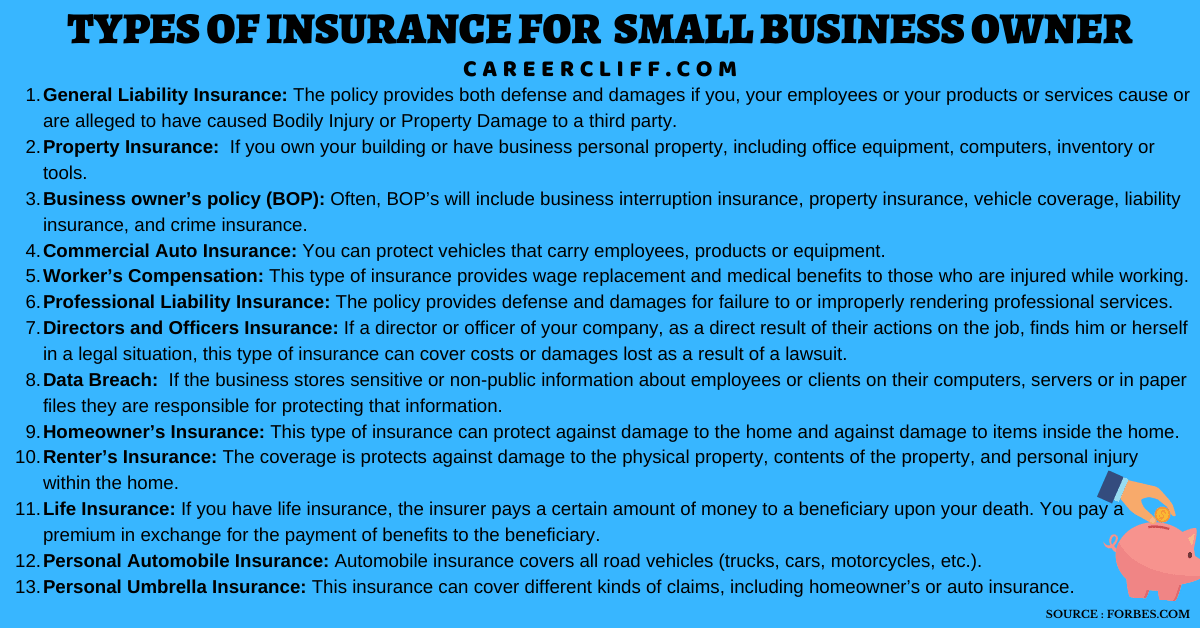

Types of Small Business Insurance

Before delving further into the complexities of business insurance, it’s crucial to clarify that I am not a specialist in insurance coverage. My insights stem from years of entrepreneurship, navigating the intricacies of business insurance, handling various claims, and experiencing firsthand the protective capabilities of insurance. This article aims to share fundamental tips on small business insurance, acknowledging the ever-changing landscape of the insurance market.

Despite the forthcoming advice, it’s essential to recognize the dynamic nature of the small business insurance market. Constant flux necessitates consultation with a reputable and knowledgeable insurance broker. This professional will engage with you, delving into the specifics of your business, asking pertinent questions, and facilitating the discovery of the most suitable small business insurance coverage for your unique needs.

Skilled Legal Responsibility Insurance: Safeguarding Against Errors

Skilled Legal Responsibility Insurance, often termed errors and omissions insurance (E&O), serves as a crucial shield for businesses, offering protection in instances where malpractice, errors, or negligence occur in the delivery of services to clients. This indispensable coverage stands as a stalwart defender, ensuring that the intricacies of professional endeavors are safeguarded against unforeseen pitfalls.

Industrial Property Insurance: Safeguarding Beyond the Tangible

Industrial Property Insurance, an integral facet of business coverage, extends its protective mantle to shield against a spectrum of potential damages. This includes events like fire, smoke, wind, hail, storms, vandalism, crime, and civil disobedience. The umbrella term “business property” encompasses not just physical assets—buildings, equipment, inventory, tools, computers—but also embraces the safeguarding of critical documents, data, and the financial repercussions of business interruption.

Employees’ Compensation Insurance: Nurturing the Workforce

A mandatory facet for businesses with a workforce, Employees Compensation Insurance takes center stage when it comes to addressing costs related to job-related injuries. This imperative coverage steps in to mitigate the financial implications of workplace injuries, underscoring its significance in fostering a workplace environment that prioritizes employee welfare. Brokers become indispensable guides, aiding in navigating state-run programs and tailored coverage solutions.

Unemployment Insurance: A Safety Net for Employees

Unemployment Insurance, another essential requirement for businesses with employees, emerges as a safety net for workers. The intricacies of this coverage vary across states, often denoted as State Unemployment Insurance (SUI) or State Unemployment Tax Act (SUTA). It forms a financial cushion for employees in the event they cease working for the business, intricately tied to payroll processes and state-specific regulations.

Disability Insurance: A Mandate for Select Locations

For businesses situated in specific locales such as California, Hawaii, New Jersey, New York, Puerto Rico, or Rhode Island, Disability Insurance becomes a compulsory addition to the coverage portfolio. A facet demanding attention, its acquisition is pivotal in meeting regulatory requisites. Brokers, acting as interpreters of legal intricacies, become key players in ensuring compliance and adequate protection.

Homeowners Insurance: Navigating Business Spaces

A common misconception lies in assuming that Homeowners Insurance inherently safeguards business interests. However, its primary focus is on personal abodes. Brokers, adept at deciphering nuanced policy details, can guide business owners in exploring the possibility of augmenting their homeowners’ coverage through riders to encapsulate specific aspects of a home-based business.

Life Insurance: Optionally Fortifying Business Continuity

Life Insurance, though optional, emerges as a strategic instrument for securing the financial future of loved ones and business partners. Its versatility is exemplified in its ability to inject financial stability into a business in the unfortunate event of the demise of a key employee or partner. Understanding the nuances of such coverage necessitates collaboration with knowledgeable insurance brokers.

Industrial Auto Insurance: Navigating Roads of Business Ventures

Industrial Auto Insurance takes the wheel in covering physical damage and bodily harm arising from accidents involving vehicles integral to business operations. Some states mandate this coverage for business vehicles, emphasizing the importance of aligning insurance portfolios with regional regulations. The tapestry of coverage intricacies unfolds, with brokers playing a pivotal role in ensuring that the vehicular dimension of business is adequately safeguarded.

Unpacking Small Business Insurance Types

Small business insurance spans a spectrum of coverage, from liability to health-related policies. Understanding the basics is pivotal for informed decision-making.

Commercial General Liability (CGL) insurance serves as a shield against claims arising from accidents, injuries, and negligence. This encompasses a wide array of scenarios, such as libel, slander, property damage, or bodily harm. Importantly, CGL can also cover the expenses incurred in a lawsuit, making it a crucial investment for every small business owner.

Product Liability insurance, on the other hand, protects businesses involved in manufacturing, distribution, or retail. This coverage becomes instrumental in mitigating financial losses resulting from product defects that lead to harm. Recognizing the specific risks associated with your business activities is key to determining the appropriate coverage needed.

Directors and Officers Insurance (D&O)

Directors and Officers Insurance (D&O) serves as a crucial facet of corporate risk management, a financial bulwark erected to shield the key decision-makers within an organization. This formidable legal liability insurance unfurls its protective wings, veiling administrators or officers from the ominous clouds of litigation that may threaten to tarnish their professional reputations. It stands as a financial fortress, ready to bear the weight of legal defenses when allegations surface, accusing these stewards of corporate destinies of actions that may have purportedly harmed the very entity they steer. Mindful Trader: Loans. Financial Services.Gifts. Stock Picking

Employment Practices Liability Insurance (EPLI)

In the dynamic theater of business operations, Employment Practices Liability Insurance (EPLI) takes center stage, an indispensable shield against the arrows of discontent that may be slung by employees, both present and past. This multifaceted insurance blueprint unveils its protective canvas when the specter of lawsuits materializes, casting shadows over the employer-employee relationship. Whether it be the ominous clouds of wrongful termination, the thunderous accusations of discrimination, the lightning strikes of sexual harassment, or the persistent drizzle of wage and hour claims, EPLI stands resolute, ready to bear the financial burdens of legal defense.

Cyber Liability (Data Breach) Insurance

In the labyrinthine world of digital landscapes, Cyber Liability Insurance emerges as the sentinel against the perils of data breaches. This specialized armor envelops an enterprise if the delicate fabric of sensitive information—business records, employee particulars, customer data—is pierced, stolen, or held hostage. It stands as a digital guardian against the chaos that may ensue from an interruption involving computer systems or data. As the shadows of cyber threats loom large, businesses are compelled to navigate this intricate realm, fortifying themselves with the assurance that Cyber Liability Insurance provides.

Consulting the Insurance Oracle

As a steward of a small business empire, the judicious course of action involves a tête-à-tête with the Insurance for Business Coverage agent, the sagacious oracle of risk management. In this ritual of enlightenment, the small business owner, akin to a seeker of arcane knowledge, delves into the nuances of required insurance policies. The insurance agent, a seasoned maestro in the symphony of risk mitigation, elucidates the harmonies and dissonances, guiding the entrepreneur through the labyrinth of protection. This bespoke consultation, a strategic alliance between the business owner and the insurance sage, unveils the tailored armor essential to fortify the enterprise against the capricious whims of unforeseen challenges. Loans & Financial Services·Credit Cards·Reporting & Repair·Tax· Insurance· Legal· B2B

Personal Umbrella Insurance

Personal Umbrella Insurance, a versatile shield of financial security, extends its protective canopy over the enterprising souls navigating the unpredictable landscapes of business ownership. In an ever-shifting terrain, this affordable and comprehensive policy becomes a beacon of assurance. A guardian angel, providing an additional layer of protection that unfurls across a myriad of unforeseen situations, is the safety net that catches a business owner when conventional safeguards fall short. In the intricate tapestry of risk management, Personal Umbrella Insurance weaves a safety net that ensures the resilience of the entrepreneurial spirit.

Health Insurance for Businesses

In the intricate dance of employee welfare, Health Insurance assumes the role of both necessity and obligation under the Affordable Care Act (ACA). A complex symphony of regulations and qualifications dictates the level of coverage mandated for the well-being of both employers and their workforce. The ACA, an additional layer in the symphony, adds complexity to the composition. Navigating this intricate terrain, akin to unraveling a convoluted can of healthcare worms, necessitates the guidance of an adept Insurance for Business Coverage broker. The health and vitality of the workforce and the financial well-being of the enterprise converge in this intricate ballet, where Health Insurance is the carefully choreographed partner.

More Interesting Articles

- Corporate Communication – Jobs, Strategy, and Functions

- Example of Transactional Leadership – Characteristics, Style, Definition

- Right Leadership Styles – Which Leadership Models Motivate a Team

- Interview Questions about Multitasking – The Best Answer

- Five Basic Generic Competitive Business Level Strategies

- Types of Goal Setting for Life in Management and Business

- Strengths of Transformational Leadership

- Creative Self Introduction Example for Students in English

- Advantages of Teamwork – Benefits of Team in Workplace Examples

- Qualities of a Bad Leader – Tricks to Hook Ineffective Leadership

- Hard Skills List – Best Job Skills in Resume for Interview Strength

- Characteristics of Entrepreneurship – Worthy Skills of Entrepreneur

- Job Interview Conversation – Questions and Answers Sample

- How to Write a Follow-up email after Phone Interview?

- New Employee Introduction Email Sample to Colleagues

- Personal Introduction | Elevator Pitch | Self Introduction Example

- True Creativity Articles – What is Creativity that Leads to Success

- Opportunities and Threats – List with Detailed SWOT Analysis Examples

- Types of Competitive Strategy Examples for Market Leaders

- Follow up email after Job Application for a Pending Job Offer